Lecture 19 Analysis of Covariance

19.1 Analysis of Covariance - ANCOVA

We consider the situation where we want to quantify the effect of a categorical variable after first adjusting for the effect of a covariate. This is called ANCOVA - analysis of covariance.

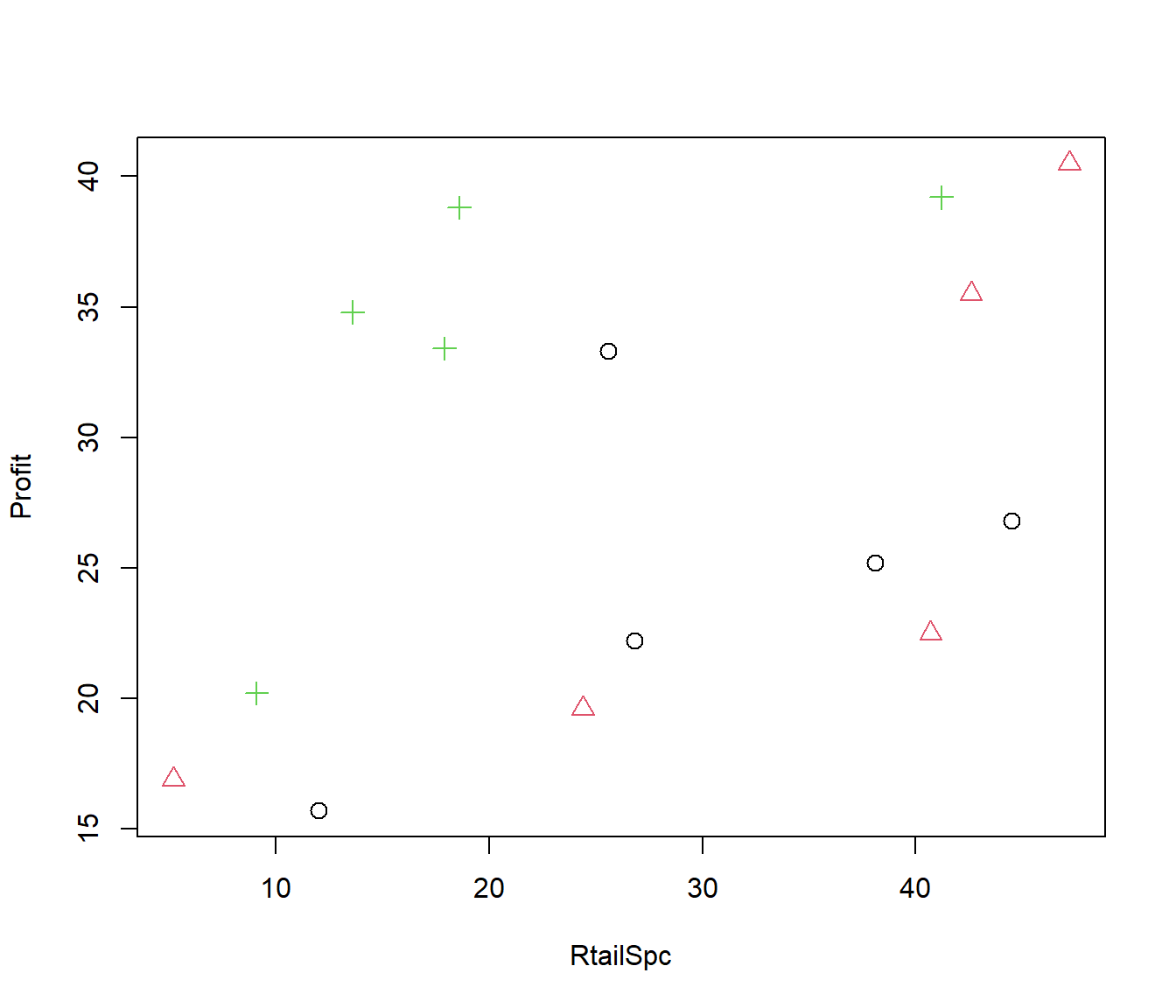

In the following example, we want to know whether the layout of shops (called ‘Arrngmt’ : shop arrangement) makes a difference to the profitability of those shops. Three different arrangements were tried, in different branches of a chain store. In order to answer the question we need to first adjust for the covariate effect ‘RtailSpc’ (retail space – the floor area of the shop).

Arrngmt Shop RtailSpc Profit Arr1 Arr2

1 1 1 26.8 22.2 1 0

2 1 2 38.1 25.2 1 0

3 1 3 44.5 26.8 1 0

4 1 4 25.6 33.3 1 0

5 1 5 12.0 15.7 1 0

6 2 6 40.7 22.5 0 1

We fit a linear model to first adjust for the covariate, then include the factor.

Retail.lm1 = lm(Profit ~ RtailSpc, data = Retail)

Retail.lm2 = lm(Profit ~ RtailSpc + as.factor(Arrngmt), data = Retail)

summary(Retail.lm2)

Call:

lm(formula = Profit ~ RtailSpc + as.factor(Arrngmt), data = Retail)

Residuals:

Min 1Q Median 3Q Max

-8.577 -3.520 -1.374 4.169 10.218

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 12.5834 4.6353 2.715 0.02012 *

RtailSpc 0.4101 0.1261 3.253 0.00769 **

as.factor(Arrngmt)2 1.2856 3.9508 0.325 0.75099

as.factor(Arrngmt)3 12.4620 4.1086 3.033 0.01138 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.225 on 11 degrees of freedom

Multiple R-squared: 0.5885, Adjusted R-squared: 0.4762

F-statistic: 5.243 on 3 and 11 DF, p-value: 0.01724Analysis of Variance Table

Model 1: Profit ~ RtailSpc

Model 2: Profit ~ RtailSpc + as.factor(Arrngmt)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 13 836.56

2 11 426.24 2 410.32 5.2945 0.02451 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1We see that the Profit is definitely related to RtailSpc, and there seems to be a significant difference between arrangements 1 and 3, but not between arrangements 1 and 2.

The anova test enables us to average the effect of the different levels of Arrngmt and conclude that, overall, Arrngment is significantly related to Profit.

19.1.1 Is there an interaction ?

We may wonder if some store arrangements make better use of space than others. That is, if the relationship between Profit and RtailSpc is altered, depending on what arrangement is being used. This means fitting an interaction model.

Call:

lm(formula = Profit ~ RtailSpc * as.factor(Arrngmt), data = Retail)

Residuals:

Min 1Q Median 3Q Max

-8.735 -3.176 -1.748 3.747 9.668

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 16.8420 8.4331 1.997 0.0769 .

RtailSpc 0.2652 0.2680 0.990 0.3482

as.factor(Arrngmt)2 -5.4642 10.9005 -0.501 0.6282

as.factor(Arrngmt)3 8.2707 10.4725 0.790 0.4500

RtailSpc:as.factor(Arrngmt)2 0.2226 0.3310 0.673 0.5181

RtailSpc:as.factor(Arrngmt)3 0.1415 0.3809 0.371 0.7189

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.715 on 9 degrees of freedom

Multiple R-squared: 0.6082, Adjusted R-squared: 0.3905

F-statistic: 2.794 on 5 and 9 DF, p-value: 0.08575Analysis of Variance Table

Model 1: Profit ~ RtailSpc + as.factor(Arrngmt)

Model 2: Profit ~ RtailSpc * as.factor(Arrngmt)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 11 426.24

2 9 405.84 2 20.41 0.2263 0.8019We see that the interaction terms are not significant, whether individually (in terms of slopes) or together (in terms of the ANOVA).

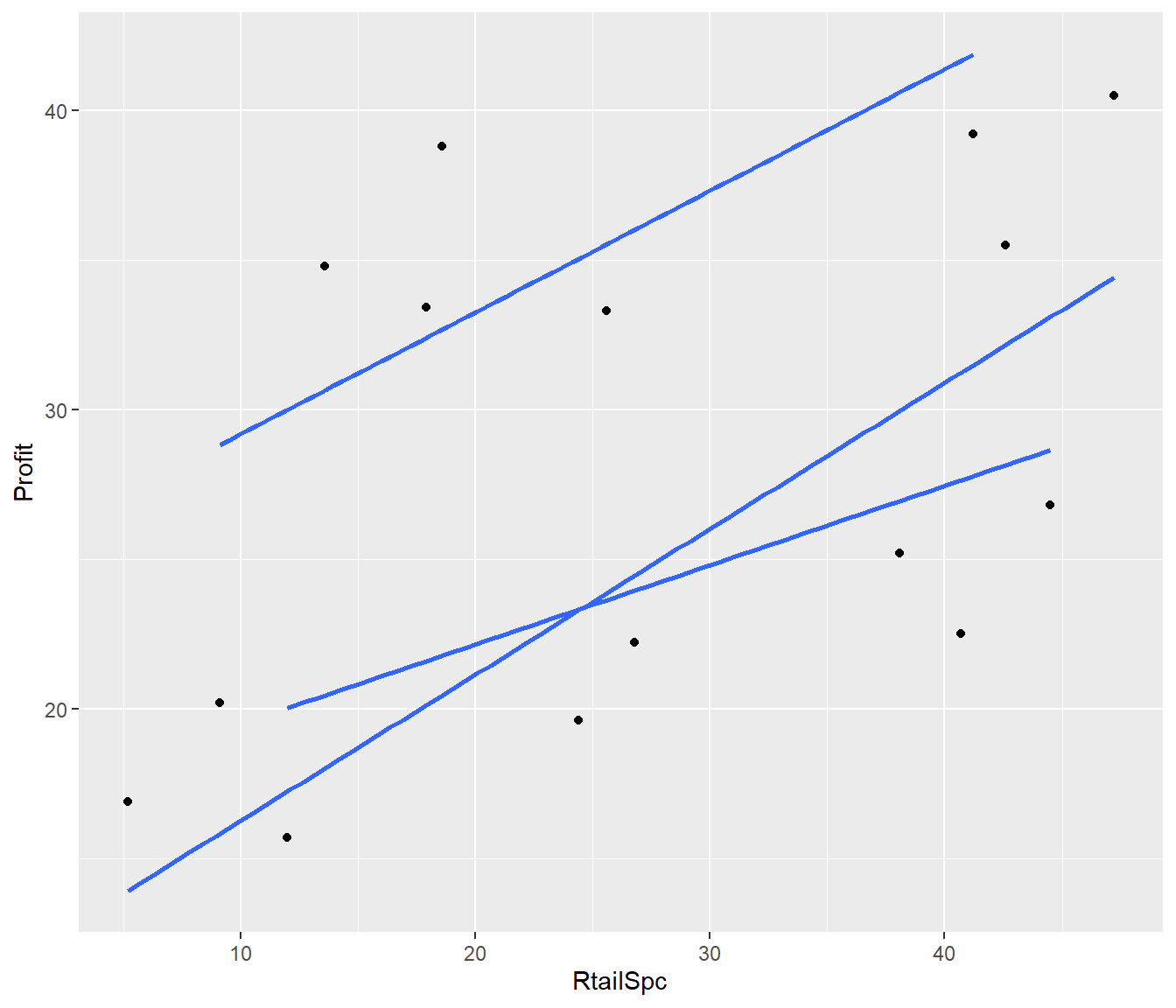

19.1.2 A Plot with Separate Lines and Symbols

You can use the following code to plot a response variable Y versus a covariate X with a group variable (factor) G

library(ggplot2)

Retail |>

ggplot(aes(x = RtailSpc, y = Profit, group = Arrngmt)) + geom_point() + geom_smooth(method = "lm",

se = FALSE)`geom_smooth()` using formula = 'y ~ x'

We see from the plot that allows for interaction, that there is little difference in slope between the three groups. If we assume parallel lines then the lines for Arrngmt 1 and 2 are very close together.

19.1.3 Writing down equations from the coefficients

Using the Summary(Retail.lm2) or the following coef(Retail.lm2) we can write down the equations for the regression lines for each group in the case of parallel lines.

For Parallel Lines

(Intercept) RtailSpc as.factor(Arrngmt)2 as.factor(Arrngmt)3

12.5833878 0.4100888 1.2855672 12.4620281 For Arrangement 1, the baseline group, the equation is \[(1) ~~~~~~~ Profit = 12.583 + 0.410 \times RtailSpc \] For Arrangement 2 and 3

\[(2) ~~~~~~~ Profit = (12.583 + 1.286) + 0.410\times RtailSpc \] \[ ~~~~~~~~~~~~~~ = 13.869 + 0.410\times RtailSpc \]

\[(3) ~~~~~~~ Profit =(12.583 + 12.462) + 0.410\times RtailSpc \] \[~~~~~~~~~~~~ = 25.045 + 0.410\times RtailSpc \] For Non-Parallel Lines

(Intercept) RtailSpc

16.8419692 0.2652391

as.factor(Arrngmt)2 as.factor(Arrngmt)3

-5.4641672 8.2706914

RtailSpc:as.factor(Arrngmt)2 RtailSpc:as.factor(Arrngmt)3

0.2226496 0.1415009 For the model with an interaction the equations are

\[(Int1) ~~~~~~~ Profit = 16.842 + 0.265 \times RtailSpc \]

\[(Int2) ~~~~~~~ Profit = (16.842 -5.464) + (0.265+ 0.223)\times RtailSpc \] \[ ~~~~~~~~~~~~~~~~ = 11.378 + 0.488\times RtailSpc \] \[(Int3) ~~~~~~~~ Profit = (16.842+ 8.271) + (0.265+ 0.142) \times RtailSpc \] \[ ~~~~~~~~~~~~~~~~ = 25.113 + 0.407\times RtailSpc \]

In the case of non-parallel lines we can check the equations by subsetting the variables. But we cannot do this for the parallel-line model.

Call:

lm(formula = Profit[Arrngmt == 2] ~ RtailSpc[Arrngmt == 2], data = Retail)

Coefficients:

(Intercept) RtailSpc[Arrngmt == 2]

11.3778 0.4879 19.2 Exercise

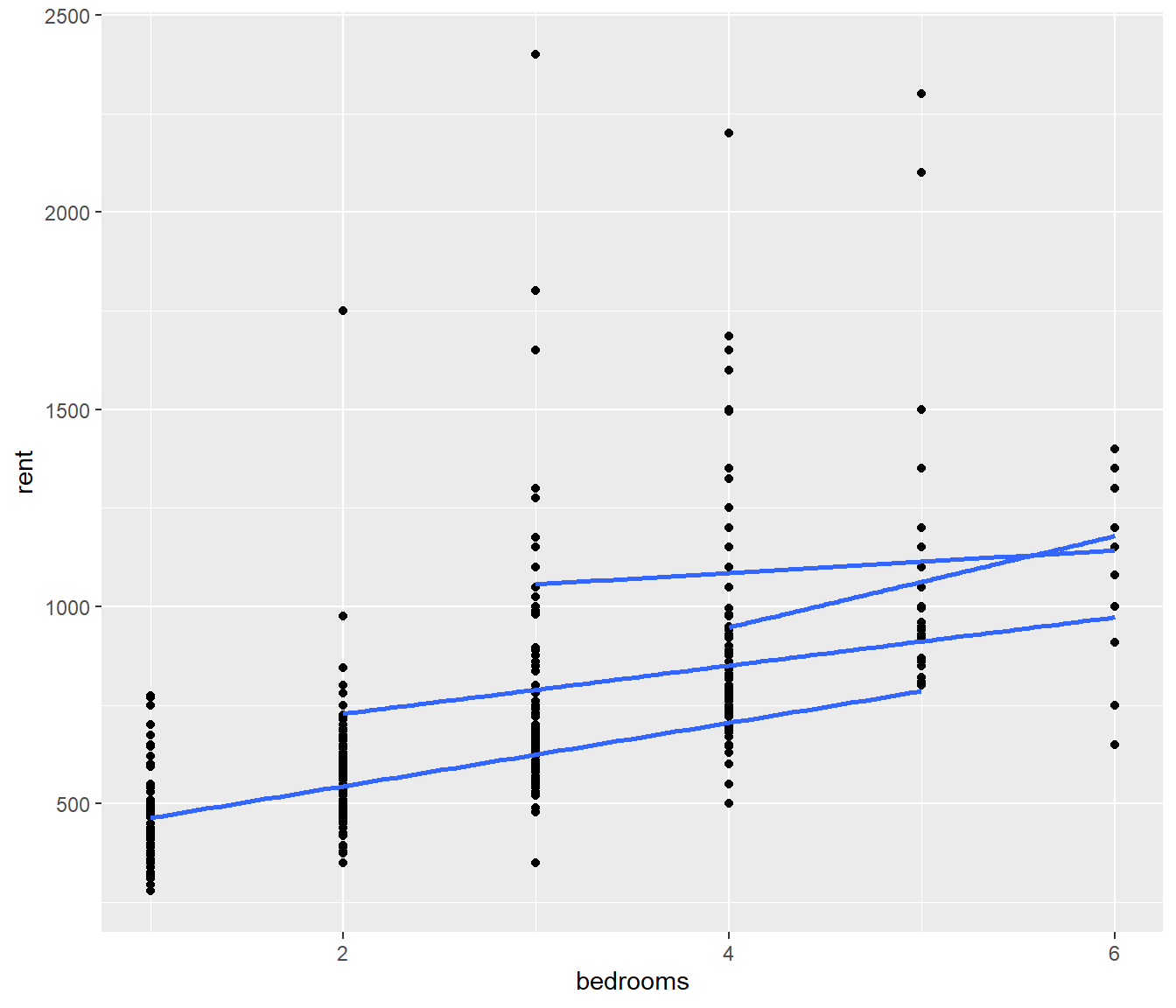

Read in the NSRent2021.csv data. The response variable is rent, and predictor variables are bedrooms and bathrooms.

- Plot to see whether the relationship between rent and bedrooms is parallel if the number of bathrooms is treated as a factor. (Note more recent houses tend to have more bathrooms)

NSrent21 |>

ggplot(aes(x = bedrooms, y = rent, group = bathrooms)) + geom_point() + geom_smooth(method = "lm",

se = FALSE)`geom_smooth()` using formula = 'y ~ x'

- Fit a parallel-lines model

lm1 = lm(rent~ bedrooms + as.factor(bathrooms))

Assuming a two-bathroom house, write down the equation relating the expected rent to the number of bedrooms.

- Fit an interaction model

lm2 = lm(rent~ bedrooms * as.factor(bathrooms))

Is the interaction model significantly better than a parallel-lines model?

Calculate the formula for the lines relating expected rent to number of bedrooms for one- and two- bathroom houses. Check your calculation by subseting the data (e.g. [bathrooms==2]) .

What is the expected rent for a house with 3 bedrooms and 2 bathrooms?

Solution

bedrooms bathrooms rent

1 1 1 280

2 1 1 280

3 1 1 295

4 1 1 295

5 1 1 310

6 1 1 320

Call:

lm(formula = rent ~ bedrooms + as.factor(bathrooms), data = NSrent)

Residuals:

Min 1Q Median 3Q Max

-462.28 -75.85 -19.69 33.51 1617.35

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 400.103 19.318 20.711 < 2e-16 ***

bedrooms 73.195 7.866 9.306 < 2e-16 ***

as.factor(bathrooms)2 162.966 18.115 8.996 < 2e-16 ***

as.factor(bathrooms)3 373.011 30.733 12.137 < 2e-16 ***

as.factor(bathrooms)4 309.962 60.276 5.142 3.52e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 172.7 on 706 degrees of freedom

Multiple R-squared: 0.5311, Adjusted R-squared: 0.5284

F-statistic: 199.9 on 4 and 706 DF, p-value: < 2.2e-16

Call:

lm(formula = rent ~ bedrooms * as.factor(bathrooms), data = NSrent)

Residuals:

Min 1Q Median 3Q Max

-392.95 -70.89 -19.89 34.77 1610.27

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 384.190 22.869 16.799 < 2e-16 ***

bedrooms 80.348 9.599 8.371 3.09e-16 ***

as.factor(bathrooms)2 222.068 60.290 3.683 0.000248 ***

as.factor(bathrooms)3 586.648 163.909 3.579 0.000368 ***

as.factor(bathrooms)4 100.400 375.193 0.268 0.789088

bedrooms:as.factor(bathrooms)2 -19.189 17.958 -1.069 0.285630

bedrooms:as.factor(bathrooms)3 -51.662 37.390 -1.382 0.167495

bedrooms:as.factor(bathrooms)4 35.390 70.561 0.502 0.616141

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 172.7 on 703 degrees of freedom

Multiple R-squared: 0.5331, Adjusted R-squared: 0.5285

F-statistic: 114.7 on 7 and 703 DF, p-value: < 2.2e-16Analysis of Variance Table

Model 1: rent ~ bedrooms + as.factor(bathrooms)

Model 2: rent ~ bedrooms * as.factor(bathrooms)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 706 21046994

2 703 20955432 3 91563 1.0239 0.3814

Call:

lm(formula = rent[bathrooms == 1] ~ bedrooms[bathrooms == 1],

data = NSrent)

Residuals:

Min 1Q Median 3Q Max

-275.23 -45.23 -9.89 34.77 1205.11

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 384.19 13.03 29.48 <2e-16 ***

bedrooms[bathrooms == 1] 80.35 5.47 14.69 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 98.39 on 443 degrees of freedom

Multiple R-squared: 0.3275, Adjusted R-squared: 0.326

F-statistic: 215.7 on 1 and 443 DF, p-value: < 2.2e-16

Call:

lm(formula = rent[bathrooms == 2] ~ bedrooms[bathrooms == 2],

data = NSrent)

Residuals:

Min 1Q Median 3Q Max

-323.21 -110.89 -59.73 34.20 1610.27

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 606.26 75.06 8.077 5.91e-14 ***

bedrooms[bathrooms == 2] 61.16 20.42 2.995 0.00309 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 232.3 on 202 degrees of freedom

Multiple R-squared: 0.04252, Adjusted R-squared: 0.03778

F-statistic: 8.97 on 1 and 202 DF, p-value: 0.003088(Intercept)

789.7348